Another Thoroughbred In Starting Gate

Back in February, Antero Resources (NYSE: AR) filed an S-1 with the SEC for the initial public offering of an MLP comprised of its midstream assets. The filing indicated that Antero Resources Midstream LLC would be converted into a limited partnership named Antero Midstream Partners LP (to trade under the ticker AM) with a valuation of up to $500 million.

But demand for new midstream IPOs has been robust — as seen most recently by Shell Midstream Partners’ (NYSE: SHLX) 45% gain on its first day of trading last week — and this may have contributed to Antero’s decision to upsize the IPO to $750 million. Units are scheduled to begin trading on the NYSE this week.

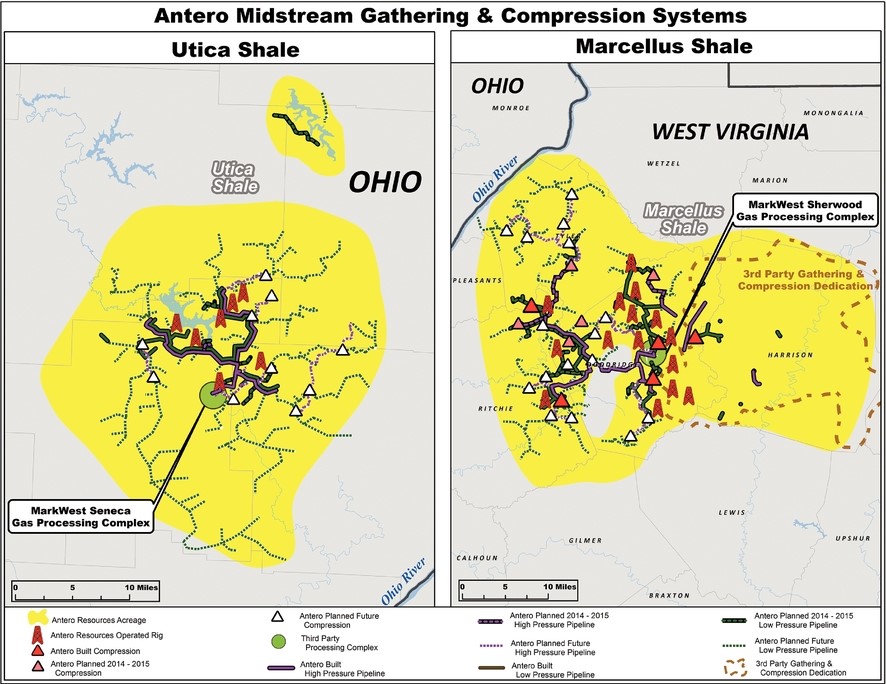

Antero Midstream Partners’ assets consist of gathering pipelines and compressor stations moving the natural gas extracted by Antero Resources. These assets are located in the liquids-rich southwestern core of the Marcellus Shale in northwest West Virginia and liquids-rich core of the Utica Shale in southern Ohio. Antero Resources is the most active driller in the Appalachian Basin with 22 operated rigs at present, including 15 operated rigs in the Marcellus Shale (where it is also the most active driller) and seven operated rigs in the Utica Shale.

Antero Midstream Partners has secured a long-term, fixed-fee contract agreement covering substantially all of Antero Resources’ current and future acreage for gathering and compression services. Antero has also granted its midstream affiliate an option to purchase fresh water distribution systems drawing from the Ohio River and several other sources for well completion operations in the Marcellus and Utica shales. These systems consist of a combination of permanent buried pipelines, portable surface pipelines, fresh water storage facilities and the associated pumping stations.

The partnership will also inherit from its parent an option to acquire a stake of up to 20% in the 800-mile Rover Pipeline project planned by Energy Transfer (NYSE: ETP) .

Antero Resources will own Antero Midstream Partners’ general partner and incentive distribution rights. The IPO is expected to distribute 37.5 million units priced between $19 and $21. The initial annualized distribution is projected to be $0.68 per unit, which would provide a midpoint yield of 3.4%. The partnership projects that it will produce $119 million in distributable cash for the twelve months ending September 30, 2015, which would provide 1.15x distribution coverage.

(Follow Robert Rapier on Twitter, LinkedIn, or Facebook.)

Portfolio Update

Shell Midstream is a Buy, But Shell Is Better

Last week, when we said we’d be adding Shell Midstream Partners (NYSE: SHLX) to the growth portfolio at its first trading day’s closing price, we didn’t count on that plan conflicting with our $29 buy below target. But SHLX went on to post a record-setting 46% first-day pop to close at $33.55. As noted last week in Stock Talk, the valuation based on trailing metrics makes the nose bleed at more than 50 times annualized distributable cash flow. It looks better considering that Shell plans to rapidly increase the distribution currently producing a modest yield of 1.9%. Effectively, SHLX is being largely priced as an option on the virtually certain dropdowns of attractive midstream assets from Shell. The downside of that rapid growth is that the distribution will within a couple of years ensure that the sponsor is entitled to 50% of future cash flows, without contributing anything toward the needed investment. We’re raising our buy below target to $35 given the strong bid likely to support the unit price in the near-term, and the strategic value of Shell’s midstream systems. But investors who don’t mind paying a little tax now in the name of long-term value should be aware that SHLX sponsor Shell (NYSE: RDS-A) is selling for 1/10th its offspring’s price based on recent cash flow, and paying a tax-advantaged ordinary dividend yield of 5.3%. It’s almost certainly the better investment over the long term. Nevertheless, SHLX is a worthwhile addition to a diversified MLP portfolio. Buy SHLX below $35.

We also plan to add Antero Midstream Partners (NYSE: AM) to the Growth Portfolio at the closing price of its first day of trading this week. As the midstream affiliate of the busiest Marcellus and Utica driller, the partnership will be the beneficiary of strong volume growth for years to come, and should be able to find new customers as well as Utica development accelerates. Buy AM below the initial target of $30.

— Igor Greenwald

Stock Talk

Grumpy Mike

Re your MLPP 11/3/14 advice “SHLX is a worthwhile addition to a diversified MLP portfolio. Buy SHLX below $35, that’s one heck of raised reco from your previous $29! I sure hope that was not a typo as I followed that revised reco and bought some below $44 near the close.

You must be logged in to post to Stock Talk OR create an account

Grumpy Mike

Correction – biught SRLX below 34, not $44

You must be logged in to post to Stock Talk OR create an account

Grumpy Mike

Last correction is SRLX is typo…should have read SHLX

Igor Greenwald

No, that’ wasn’t a typo. It’s a buy below $35. As mentioned in the article, the valuation is very expensive. But the asset base is excellent, the distribution growth should be rapid and the demand for this offering was telling.

You must be logged in to post to Stock Talk OR create an account

You must be logged in to post to Stock Talk OR create an account

Add New Comments

You must be logged in to post to Stock Talk OR create an account